Key Points :

- Modern war spreads through global markets, supply chains, and energy systems, making prolonged conflict economically unsustainable.

- The Strait of Hormuz is a critical vulnerability, and the conflict caused an unprecedented oil supply disruption.

- The war triggered both rising inflation and slowing global growth, forcing GDP downgrades.

- The April 8, 2026 ceasefire was an economic necessity to prevent infrastructure loss and a global recession.

- Today, economic systems, not battlefields, determine war sustainability, making peace structurally essential.

Executive Summary

The ongoing conflict involving Iran, the United States, Israel, and regional actors is often interpreted through a military-strategic lens. This paper argues that its defining characteristic is systemic economic disruption across interconnected global markets. Drawing on pre-war economic indicators, real-time energy market shocks, and early macroeconomic responses, this study demonstrates that the conflict rapidly evolved into a global economic stress event with stagflationary risk. The April 8, 2026 ceasefire is therefore best understood not as a tactical pause, but as a rational economic intervention to prevent cascading financial instability.

The core finding is clear:In a highly integrated global economy, prolonged high-intensity conflict in critical energy corridors is structurally unsustainable for all actors.

War Beyond the Battlefield

While headlines focus on strategic maneuvers, the foundational stability of nations and the global order rests on economics. Modern warfare no longer operates in isolation.

Unlike 20th-century conflicts, today’s wars propagate through financial markets, energy systems, supply chains, and inflation dynamics.

In the modern era, war is no longer a localized zero-sum game; it is a systemic shock. This analysis uses available economic data to prove that prolonged conflict in the Persian Gulf is an unsustainable strategy for all parties. The Persian Gulf, home to the Strait of Hormuz, through which roughly one-fifth of global oil flows, represents a single point of systemic vulnerability. Any disruption transforms regional conflict into a global macroeconomic event.

This analysis evaluates the Iran conflict through this lens, arguing that economic constraints -not military limitations- define the ceiling of escalation.

Iran’s Pre-War Economic Trajectory: A Study in Fragility

Prior to the outbreak of active hostilities in early 2026, Iran’s economy was already exhibiting signs of profound structural deterioration, marked by entrenched inefficiencies, external constraints, and severely limited fiscal flexibility. Rather than entering the conflict from a position of resilience, Tehran faced a compounding set of economic vulnerabilities that had accumulated over more than a decade of sustained pressure.

A central driver of this decline was the cumulative impact of international sanctions, particularly secondary sanctions targeting Iran’s energy sector. These measures significantly constrained the country’s ability to export oil at scale, depriving the state of its primary source of foreign currency earnings. Estimates suggest that Iran forfeited between $300 billion and $450 billion in potential oil revenues over this period, resulting in depleted reserves and diminished capacity to stabilize its economy or finance strategic priorities.1

Simultaneously, Iran was grappling with a severe monetary and inflationary crisis. The Iranian rial had already undergone a dramatic collapse, losing more than 90 percent of its value by 2018, and continued to weaken in subsequent years. By late 2025, inflation had surged beyond 60–70 percent, eroding household purchasing power and contributing to widespread economic hardship. This persistent inflationary environment not only undermined consumer confidence but also constrained domestic investment and long-term economic planning.2

Macroeconomic indicators further reflected a trajectory of contraction even before the onset of war. Forecasts for 2026 pointed to negative growth of approximately -2 percent, signaling a stagnating economy with limited capacity for recovery. Crucially, these projections did not fully account for the fiscal burden of sustained military operations, which would inevitably redirect state resources away from already strained civilian sectors.3

Taken together, these conditions illustrate that Iran entered the conflict with minimal economic resilience. The convergence of sanctions-induced revenue losses, currency instability, high inflation, and negative growth left the country without the financial depth necessary to sustain a prolonged, high-intensity conflict without incurring severe internal economic consequences.

Immediate Economic Shock of the War (Feb-Mar 2026)

The initial phase of the war produced the most severe market volatility observed in the energy sector in recent history, with disruption effects rapidly concentrated in global oil flows and pricing mechanisms. What emerged was not a gradual adjustment, but a systemic shock that effectively destabilized one of the most critical pillars of the international economy.

Energy Markets: The Systemic Seizure

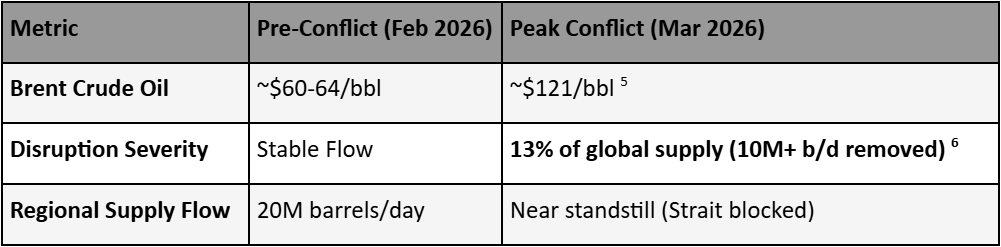

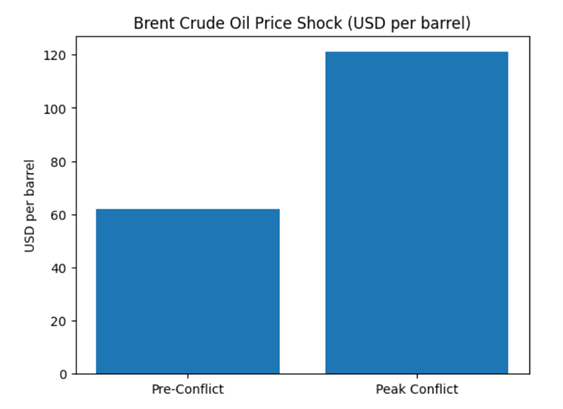

In its early assessment of the crisis, the International Energy Agency characterized the opening weeks of the conflict as “the largest oil supply disruption in modern history,” underscoring the scale and immediacy of the shock to global energy infrastructure. The epicenter of this disruption was the Strait of Hormuz, a critical maritime artery through which a substantial portion of global oil trade flows.4

As tensions escalated and maritime traffic became increasingly constrained, energy markets reacted with extreme price volatility. Brent crude prices surged dramatically from a baseline range of approximately $60-64 per barrel to a peak near $121 per barrel, reflecting both supply fears and speculative pressure. At the same time, physical supply flows through the region experienced an unprecedented contraction, moving from roughly 20 million barrels per day under normal conditions to near standstill levels as transit through the Strait was effectively obstructed. This dual shock, simultaneous price escalation and volume collapse, represented a rare convergence of market stress factors, amplifying global uncertainty and accelerating broader economic contagion.5

Global Inflation and Growth Degradation

The immediate aftermath of the price shock triggered a broad-based deterioration in global economic performance, as rising energy and transportation costs cascaded through supply chains and consumption patterns. What began as a disruption in commodity markets rapidly translated into systemic pressure on output, investment, and household demand across both advanced and emerging economies.

By April 7, 2026, the International Monetary Fund had already signaled a downward revision of global growth expectations for the year, reflecting the speed and severity of the unfolding economic strain. Preliminary assessments indicated that global GDP growth would likely decline by approximately 0.3 percentage points in 2026. The adjustment was particularly pronounced in the United States, where growth projections were revised sharply downward, from an earlier estimate of 2.4 percent to just 1.4 percent, underscoring the sensitivity of even large, diversified economies to sustained energy price volatility.8

At the consumer level, the inflationary surge translated directly into diminished purchasing power. Elevated energy prices, compounded by increased logistics and transportation costs, exerted upward pressure on the price of goods and services across the board. In the United States, prolonged exposure to these conditions was projected to erode real purchasing power by approximately 0.6 percent. While this figure may appear modest in isolation, its broader implications are significant, as reduced consumer spending capacity can dampen aggregate demand, slow economic momentum, and reinforce the cycle of weakened growth.9

The April 8 Ceasefire

The trajectory of the conflict underwent a decisive shift on April 8, 2026, with the announcement of a two-week, diplomatically mediated ceasefire. While framed in political and security terms, the timing and alignment of key actors strongly indicate that the decision was driven, at its core, by converging economic imperatives. Faced with mounting evidence of systemic strain, all parties appeared to recognize the accelerating risk of a stagflationary spiral (characterized by rising inflation, declining output, and financial instability), that could rapidly evolve into a broader global recession if left unchecked.

By early April, the economic signals had become increasingly difficult to ignore. Oil prices had surged to approximately $121 per barrel at their peak, reflecting acute supply concerns and market panic. Although prices began to ease modestly toward the mid-$90 range, volatility remained elevated, undermining market confidence and long-term planning. This instability had immediate second-order effects, particularly in advanced economies such as the United States, where uncertainty in energy markets translated into hesitation in capital investment and a noticeable slowdown in service-sector expansion, including hiring. In effect, the persistence of volatility, not merely the price level itself, became a key constraint on economic activity.9

At the same time, the risk of irreversible structural damage introduced a new and urgent dimension to decision-making. On April 7, Donald Trump publicly threatened to “decimate every bridge and power plant” in Iran, signaling a potential escalation toward widespread infrastructure targeting. Had such actions been carried out, the economic consequences would likely have extended far beyond short-term disruption, tipping into long-term systemic collapse. Critical energy and transport infrastructure, particularly in and around the Gulf, would have faced destruction that could not be quickly repaired, thereby transforming a volatile but reversible crisis into a prolonged supply shock with enduring global repercussions. In this context, the ceasefire can be interpreted as a strategic pause designed not only to de-escalate militarily, but also to preserve infrastructure whose continued functionality is essential to both regional stability and global energy flows.

Regional dynamics further reinforced the economic logic behind the ceasefire. The vulnerability of the Strait of Hormuz had become a central pressure point, with the effective bottlenecking of one of the world’s most critical energy transit routes. Key regional actors, including Saudi Arabia and United Arab Emirates, found themselves confronting a stark trade-off between strategic objectives and economic survival. The potential loss of up to 10 million barrels per day in exports, on a sustained basis, posed an existential threat to their fiscal stability and long-term economic planning. Under such conditions, the costs of continued escalation began to outweigh the perceived benefits, contributing to a convergence of interests in favor of de-escalation.9

Taken together, these factors suggest that the April 8 ceasefire was less a diplomatic breakthrough than an economically rational recalibration. It reflects a moment in which the cumulative weight of market instability, infrastructure risk, and regional economic exposure compelled all sides to step back from the brink, at least temporarily, in order to prevent a far more damaging and potentially uncontrollable economic outcome.

Regional and United States Economic Fallout

The economic consequences of the conflict were not confined to global aggregates, where structural dependencies and geographic exposure amplified the shock. Nowhere was this more evident than in the Gulf, where the very states that benefit from hydrocarbon exports found themselves acutely vulnerable to supply chain disruptions and trade bottlenecks.

For the Gulf Cooperation Council (GCC) states, the crisis exposed a fundamental asymmetry between energy wealth and food security. Despite their status as major oil and gas exporters, countries such as Saudi Arabia and the United Arab Emirates rely heavily on imported food, with as much as 70 percent of consumption sourced from abroad. As maritime routes became increasingly unstable, particularly in and around the Strait of Hormuz, supply chains were disrupted and import costs surged. The result was a sharp escalation in food prices, with staple goods increasing between 40 and 120 percent during March and April 2026. This dynamic placed immediate pressure on domestic stability, as governments were forced to absorb higher subsidy costs while managing inflation-sensitive populations.10

At the same time, the very lifeblood of GCC economies, the export of hydrocarbons, faced unprecedented constraints. The effective bottlenecking of the Strait of Hormuz curtailed the flow of oil and gas to global markets, stalling export volumes and, by extension, government revenues. Given the centrality of hydrocarbon income to fiscal planning, this disruption posed a direct threat to budgetary stability, sovereign investment programs, and long-term economic diversification initiatives. In essence, the region confronted a dual shock: rising import costs alongside constrained export capacity.6

The United States, while more insulated due to its diversified economy and domestic energy production, was not immune to the secondary effects of the crisis. One of the most immediate impacts was visible at the consumer level, where gasoline prices rose steadily (by approximately 5 to 10 cents per day), during periods of peak market volatility. This rapid increase fed directly into broader inflationary pressures, affecting transportation costs, goods pricing, and household budgets across the country.10

Beyond inflation, the more significant concern for the U.S. economy was the growing risk of recession under a prolonged high-price energy scenario. Economic modeling suggested that if oil prices were to escalate toward the $150–$170 per barrel range, consistent with a worst-case escalation scenario, the resulting demand destruction and cost pressures would likely tip not only the United States but the global economy into recession. In this context, the two-week ceasefire assumes added significance, as it serves to cap immediate escalation risks and stabilize energy markets, thereby reducing the probability of a severe downturn.11

Conclusion – The Rational Case for Peace

The overarching conclusion of this analysis is that modern, globalized warfare is inherently self-defeating when measured against the realities of economic interdependence. In contrast to earlier eras, where territorial gains or military attrition could decisively shape outcomes, contemporary conflicts are constrained by the immediate and far-reaching consequences they impose on interconnected markets, supply chains, and financial systems. In this context, the most compelling argument for de-escalation is not ideological or strategic, but fundamentally economic: the immutable logic of survival within a fragile global system.

The events surrounding the April 8 ceasefire underscore this dynamic with particular clarity. The decision to halt hostilities, even temporarily, reflects a convergence of rational self-interest among all actors involved. At the center of this calculation lies the urgent need to restore the flow of commerce, especially through critical chokepoints such as the Strait of Hormuz, whose disruption had already demonstrated the capacity to destabilize global energy markets and trigger cascading economic effects. In this sense, the ceasefire is less a diplomatic concession than a systemic necessity, an acknowledgment that continued escalation would impose costs exceeding any conceivable strategic gain.

More broadly, the Iran conflict illustrates a structural transformation in the nature of warfare itself. Economic systems have emerged as the primary determinant of a conflict’s sustainability, effectively superseding traditional battlefield metrics. Military operations can no longer be evaluated in isolation from their macroeconomic consequences; instead, they are embedded within a global framework where capital flows, commodity prices, and supply chain integrity impose hard limits on escalation.

Within this framework, the April 8 ceasefire can be understood as a mechanism of market stabilization, aimed at calming volatility and restoring a degree of predictability to global energy and financial systems. Simultaneously, it functions as a risk containment strategy, designed to prevent localized conflict from metastasizing into a broader economic crisis. Perhaps most importantly, it serves as a precursor to necessary economic normalization, creating the conditions under which trade flows, investment decisions, and fiscal planning can begin to recover.

Ultimately, sustained peace is not merely a normative or humanitarian objective; it is a structural requirement of the modern international system. Without it, the cumulative pressures of inflation, disrupted trade, and declining output risk converging into systemic economic breakdown. In a deeply interconnected global economy, the cost of war is no longer confined to the battlefield, it is borne universally, and it is increasingly unsustainable.

Sources

- Estimate based on multiple energy market analyses (e.g., Kpler, Vortexa) covering 2018–2025 sanctions periods.

- World Bank. (2025). Iran Economic Monitor, Fall 2025.

- International Monetary Fund. (2025). World Economic Outlook, October 2025.

- International Energy Agency. (2026, March). Monthly Oil Market Report: Special Conflict Supplement.

- Data retrieved from ICE Futures Europe and CME Group (March 15, 2026, peak).

- U.S. Energy Information Administration (EIA). (2026). World Oil Transit Chokepoints: Strait of Hormuz Analysis.

- International Monetary Fund (IMF). (2026, April 7). Statement on the Global Economic Outlook regarding the Middle East Conflict.

- Revised consensus projection based on major institutional downgrades (e.g., Goldman Sachs, JPMorgan, April 2026).

- Bureau of Economic Analysis (BEA). (2026). Personal Income and Outlays reports (Mar 2026, preliminary data).

- Local media reports and market data from GCC food importing hubs (Dubai, Riyadh, Doha, April 2026).

- Analysis cited from major global financial institutions and economic research forums (e.g., Brookings, Atlantic Council) during late March 2026.

click here to download as PDF.